GLP-1 medications, such as Semaglutide, Liraglutide, and Dulaglutide, have become increasingly popular for managing type 2 diabetes and weight loss. With their high cost, one of the most common questions people ask is: Does health insurance cover GLP-1?

The answer isn’t simple. Coverage depends on your insurance type, your medical condition, and whether your plan deems the medication medically necessary. This guide will help you understand insurance coverage for GLP-1, potential costs, and ways to maximize your benefits.

Understanding whether health insurance covers GLP-1 medications is essential for anyone considering these treatments for diabetes or weight management. Coverage is not guaranteed and often depends on the type of insurance plan you have, the specific medication prescribed, and whether your healthcare provider can demonstrate medical necessity.

Many private insurance plans provide coverage for GLP-1 drugs when used to manage type 2 diabetes, but coverage for weight loss purposes is less common. Medicare Part D may cover certain GLP-1 medications, but typically only for diabetes, leaving weight management claims denied. Medicaid coverage varies significantly by state, meaning some patients may receive full support while others face out-of-pocket expenses.

Even when insurance approves coverage, prior authorization is often required, which can take time and require detailed medical documentation. Patients are encouraged to review their plan’s formulary to see which GLP-1 drugs are included and to explore patient assistance programs or manufacturer discounts to offset costs. Mail-order pharmacies can sometimes offer lower copays, and consulting with a healthcare provider can help ensure the most cost-effective approach. Understanding these factors before starting therapy can help reduce surprises and financial strain.

Ultimately, proactive planning, careful documentation, and open communication with your insurer are key to getting GLP-1 coverage and ensuring the treatment fits within your healthcare budget.

1. What Are GLP-1 Medications?

GLP-1 medications, or glucagon-like peptide-1 receptor agonists, are a class of injectable drugs designed to help regulate blood sugar and control appetite. They mimic the action of the body’s natural GLP-1 hormone, which slows gastric emptying and promotes insulin secretion after meals.

These medications are primarily prescribed for people with type 2 diabetes, but some are also approved for weight management in patients with obesity. Common GLP-1 drugs include Semaglutide, Liraglutide, and Dulaglutide, each with specific dosing schedules and treatment goals.

GLP-1 therapy has been shown to improve blood sugar control, support weight loss, and reduce the risk of cardiovascular complications in certain patients. Despite their benefits, these medications can be expensive, making insurance coverage a crucial factor for many individuals.

They are administered via subcutaneous injection, usually once weekly or daily depending on the medication. Side effects may include nausea, vomiting, or gastrointestinal discomfort, which usually improve over time with proper monitoring.

Understanding the role of GLP-1 medications is key for anyone considering treatment, as it affects decisions about insurance coverage, cost management, and overall treatment planning. Working closely with a healthcare provider ensures the medication is used safely and effectively.

GLP-1, or glucagon-like peptide-1 receptor agonists, are injectable medications that help regulate blood sugar, slow gastric emptying, and control appetite. They are approved for:

- Type 2 diabetes management

- Obesity treatment (in some medications)

Popular GLP-1 Medications

| Medication | Brand Name | FDA Approval | Typical Use |

| Semaglutide | Ozempic, Wegovy | 2017 (diabetes), 2021 (weight) | Diabetes & Weight Loss |

| Liraglutide | Victoza, Saxenda | 2010 (diabetes), 2014 (weight) | Diabetes & Weight Loss |

| Dulaglutide | Trulicity | 2014 | Diabetes Management |

Key Point: These medications are effective but expensive, making insurance coverage critical for affordability.

2. How Health Insurance Coverage Works?

Understanding how health insurance coverage works for GLP-1 medications is essential before starting treatment. Coverage is determined by your insurance plan type, the medical purpose of the prescription, and whether the insurer considers the medication medically necessary.

Most private insurance plans cover GLP-1 drugs for type 2 diabetes, but coverage for weight loss is often limited or excluded. Insurance companies typically require prior authorization, meaning your doctor must submit documentation proving the medication is essential for your health.

Medicare Part D may cover some GLP-1 medications for diabetes management, but rarely for obesity-related use. Medicaid coverage varies widely from state to state, so eligibility and out-of-pocket costs can differ significantly.

It’s important to check your plan’s formulary, which lists covered medications and associated copays. Some plans may require you to try alternative treatments first before approving GLP-1 coverage, a process known as step therapy.

By understanding these rules and requirements, patients can better navigate the approval process, reduce delays, and ensure they receive the treatment they need at the lowest possible cost.

Health insurance coverage depends on the type of plan you have and how the insurance company categorizes GLP-1 medications.

1. Private Insurance

- Most private insurance plans cover GLP-1 medications for type 2 diabetes, but coverage for weight loss is often limited.

- Prior authorization is commonly required to confirm medical necessity.

- Coverage and copays vary widely by plan and pharmacy.

2. Medicare Coverage

- Medicare Part D may cover GLP-1 medications for diabetes management.

- Obesity-related coverage is rarely provided.

- Costs can still be high even if the medication is covered.

3. Medicaid Coverage

- Medicaid coverage varies by state.

- Some states provide partial coverage for diabetes but exclude coverage for weight management.

Tip: Always check the insurance formulary before starting GLP-1 therapy to avoid surprises.

3. Out-of-Pocket Costs Without Insurance

GLP-1 medications can be expensive when paying out-of-pocket, often costing hundreds or even over a thousand dollars per month. Prices vary depending on the brand, dosage, and pharmacy, which can make long-term treatment a significant financial burden.

For example, Semaglutide may range from $900 to $1,200 monthly, while Liraglutide often costs between $800 and $1,100. Dulaglutide tends to be slightly less expensive, averaging $500 to $900 per month.

Patients without insurance coverage may also face additional costs for doctor visits, lab tests, and monitoring while on GLP-1 therapy. These combined expenses can make managing diabetes or weight loss challenging for many individuals.

To reduce costs, some patients explore manufacturer coupons, patient assistance programs, or discount pharmacies. Mail-order pharmacies can sometimes provide lower prices, especially for long-term prescriptions.

Planning ahead and budgeting for these costs is crucial if insurance does not cover GLP-1 medications. Speaking with your healthcare provider about cost-saving options can help make treatment more affordable and sustainable.

GLP-1 medications are expensive without insurance. Here’s a rough breakdown of monthly costs:

- Semaglutide (Ozempic/Wegovy): $900–$1,200

- Liraglutide (Victoza/Saxenda): $800–$1,100

- Dulaglutide (Trulicity): $500–$900

Ways to Reduce Costs

- Use manufacturer coupons or patient assistance programs

- Consider mail-order pharmacies for lower prices

- Ask your doctor about generic alternatives when available

4. Steps to Maximize GLP-1 Insurance Coverage

Maximizing insurance coverage for GLP-1 medications starts with understanding your plan’s requirements. Most insurers require prior authorization, so your doctor must provide detailed documentation showing medical necessity.

Keeping thorough records of your medical history, lab results, and prior treatment attempts can strengthen your case for approval. Some plans may require step therapy, meaning you must try other medications first, so being prepared can save time.

Check your insurance formulary to ensure the specific GLP-1 medication is listed, and confirm any restrictions on dosage or pharmacy use. Using specialty or mail-order pharmacies can sometimes reduce copays and simplify refills.

If coverage is denied, don’t hesitate to appeal with supporting documentation from your healthcare provider. Additionally, explore manufacturer assistance programs or coupons, which may offset costs even if insurance partially covers the medication.

This infographic illustrates the key steps to maximize GLP-1 coverage through health insurance.

Proactive planning and clear communication with your doctor and insurer are key to maximizing your chances of approval and minimizing out-of-pocket expenses.

- Obtain Prior Authorization: Most insurance companies require documentation from your healthcare provider.

- Document Medical Necessity: Include lab results, BMI records, and history of failed treatments.

- Check Formulary Updates: Ensure your medication is on the plan’s covered list.

- Appeal Denials: You have the right to appeal if coverage is denied.

- Use Specialty Pharmacies: They often handle prior authorizations and may reduce costs.

5. Pros and Cons of Using Insurance for GLP-1

Using insurance to cover GLP-1 medications offers several benefits, including reduced out-of-pocket costs and easier access to specialty pharmacies. However, there are also drawbacks, such as potential delays due to prior authorization and limited coverage for weight management. Understanding these advantages and disadvantages can help you make informed decisions about your treatment plan.

The table below summarizes the main pros and cons of using health insurance for GLP-1 medications, helping you weigh the benefits and potential challenges.

| Pros | Cons |

| Reduced out-of-pocket costs | Approval may require multiple steps |

| Encourages long-term adherence | Coverage may exclude obesity-related use |

| Access to specialty pharmacies | Copays can still be high |

6. Real-Life Case Studies

Consider Emily, a 52-year-old with type 2 diabetes whose doctor prescribed Semaglutide. Her health insurance initially required prior authorization, but after submitting her medical history and lab results, her coverage was approved within two weeks. This shows how proper documentation can speed up the health insurance approval process.

Michael, a 40-year-old seeking GLP-1 for weight management, faced a denial because his health insurance plan only covers the medication for diabetes. He was able to reduce costs by using manufacturer coupons while exploring alternative therapies, highlighting that health insurance limitations don’t always mean there’s no way to access treatment.

These cases demonstrate that medical necessity, thorough documentation, and persistence can make a big difference when working with health insurance providers. Collaborating closely with your healthcare provider and understanding your health insurance policy can help avoid delays and unexpected out-of-pocket expenses.

Case 1: Sarah, 45, has type 2 diabetes and private health insurance. Her doctor submitted prior authorization for Semaglutide, and her coverage was approved after two weeks. Her monthly copay through health insurance was $50.

Case 2: John, 38, has obesity and no prior diabetes diagnosis. He tried to get Wegovy covered, but his health insurance denied the claim. He used manufacturer coupons to lower his out-of-pocket costs while exploring other options.

Lesson: Successful coverage depends on medical necessity, insurance plan policies, and persistence. Understanding how your health insurance works and actively managing the process can make GLP-1 therapy more accessible and affordable.

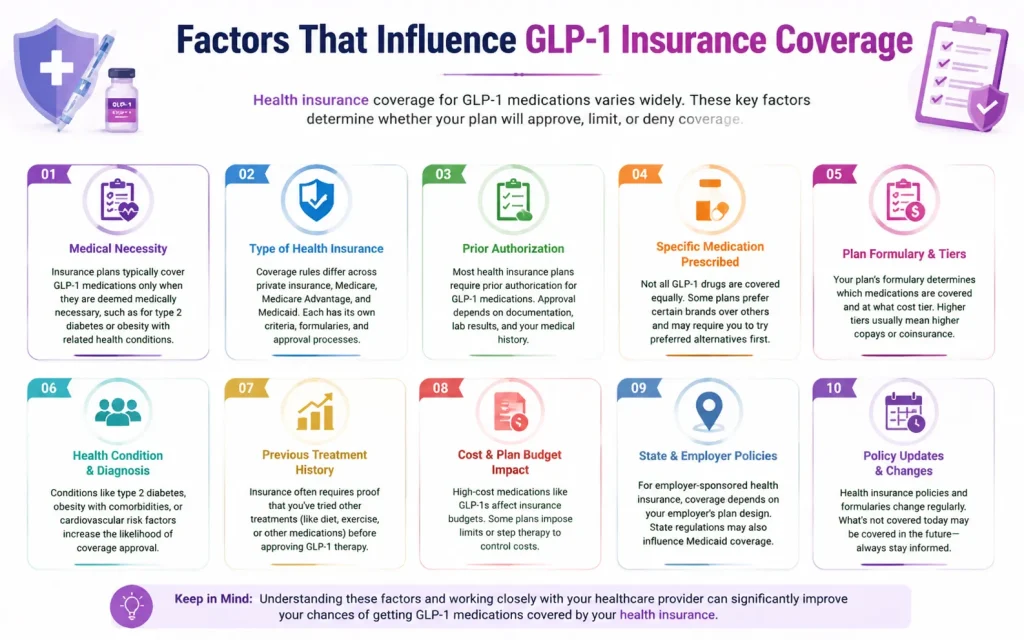

7. Factors That Influence Coverage

Several factors can influence whether your health insurance covers GLP-1 medications. First, the type of insurance plan you have—HMO, PPO, Medicare, or Medicaid—can affect what is covered and how much documentation is required.

Your medical condition plays a critical role. Plans are more likely to cover GLP-1 for type 2 diabetes than for weight management, as insurers prioritize treatments deemed medically necessary.

The specific medication prescribed also matters. Some GLP-1 drugs may be included on your plan’s formulary, while others are excluded or require prior approval.

Insurance companies may require prior treatment attempts, known as step therapy, before approving GLP-1 coverage. Providing comprehensive medical records, including lab results, BMI, and treatment history, can improve approval chances.

This infographic illustrates the main factors that determine whether GLP-1 medications are covered by health insurance.

Other factors include state-specific Medicaid rules, prescription dosage, pharmacy network restrictions, and co-pay tiers. Being aware of these elements helps you anticipate potential hurdles.

By understanding these variables and working closely with your healthcare provider, you can increase the likelihood of successful approval and reduce delays in accessing GLP-1 therapy.

- Insurance Plan Type: HMO, PPO, Medicare, or Medicaid

- Medical Condition: Diabetes vs. Obesity

- Medication Formulary: Only certain GLP-1 brands may be covered

- Documentation: Adequate medical records improve approval chances

8. Alternative Options If Coverage is Denied

If your insurance denies coverage for GLP-1 medications, there are still ways to access treatment or reduce costs. One option is to explore manufacturer assistance programs, which may provide discounts or free medication for eligible patients.

Some patient support organizations offer coupons or cost-sharing help for GLP-1 drugs. Participating in clinical trials can also give access to these medications at little or no cost while contributing to research.

For those without coverage, other diabetes medications may be more affordable and still help manage blood sugar effectively, though they may not have the same weight-loss benefits. Combining medication with lifestyle changes, such as diet and exercise, can improve outcomes and sometimes reduce the required dosage.

Consulting your healthcare provider about these alternatives ensures you receive effective treatment while managing costs. Being proactive and informed can make a significant difference if coverage is denied.

- Manufacturer assistance programs

- Patient support groups for discounts

- Clinical trials offering GLP-1 treatments

- Lifestyle interventions alongside lower-cost medications

Conclusion

Navigating health insurance coverage for GLP-1 medications can feel complicated, but understanding Navigating health insurance coverage for GLP-1 medications can feel complex, but understanding your health insurance plan and available options makes a big difference. Coverage often depends on medical necessity, the specific GLP-1 medication prescribed, and the type of health insurance you have.

Most health insurance plans require prior authorization, so having thorough medical documentation, lab results, and treatment history is essential. For patients without insurance coverage, costs can be high, but manufacturer assistance programs and mail-order pharmacies can help offset expenses and make treatment more affordable.

Even if your health insurance claim is denied initially, you can appeal with proper documentation or explore alternative medications to ensure effective treatment. Being proactive, maintaining clear communication with your healthcare provider, and understanding the rules of your health insurance policy are key to success.

By following these strategies, patients can maximize their chances of approval, manage costs effectively, and achieve their desired health outcomes with GLP-1 therapy.

Key Takeaways for Health Insurance and GLP-1 Coverage:

- Coverage depends on medical necessity and your health insurance plan.

- Private insurance, Medicare, and Medicaid vary widely in what they cover.

- Prior authorization is almost always required by health insurance providers.

- Costs without insurance are high, so explore assistance programs.

- Check your plan’s formulary before starting GLP-1 therapy.

- Document your medical history carefully for health insurance purposes.

- Appeals are possible if your health insurance claim is denied.

- Using mail-order and specialty pharmacies can reduce costs.

- Alternatives exist if health insurance coverage is not approved.

With proper planning, documentation, and knowledge of your health insurance options, you can maximize your chances of getting GLP-1 coverage while keeping costs manageable.

Frequently Asked Questions (FAQs)

1. Does Medicare cover GLP-1 for weight loss?

Generally, no. Coverage is primarily for diabetes.

2. Are all GLP-1 drugs covered by insurance?

No. Coverage depends on the plan and the formulary.

3. Do I need a referral or prior authorization?

Often, yes. Insurance companies require documentation from your doctor.

4. Can insurance deny coverage for GLP-1?

Yes, particularly if prescribed for obesity rather than diabetes.

5. Is there a generic GLP-1 available?

Most GLP-1 drugs are brand-name only.

6. How much will my copay be?

Varies by plan, ranging from $30–$150 per month.

7. Does Medicaid cover GLP-1 for diabetes?

Coverage varies by state. Some Medicaid programs provide partial coverage.

8. Are there alternatives if GLP-1 is not covered?

Other diabetes medications may be available, though their effectiveness for weight loss may vary.